Interest rates, inflation, and growth

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

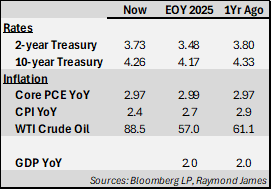

The U.S. market story this year has been a tug-of-war between sticky inflation, slower growth, and resilient risk appetite. For fixed-income investors, that mix has produced more narrative movement than the 10-year Treasury itself. The 10-year closed at 4.26% on Friday, April 17, versus 4.17% at year-end 2025, while the 2-year moved from 3.48% to 3.73%. In other words, rates have drifted higher year to date, but not explosively so; the market has spent much of the year testing whether inflation, growth, or Fed patience would prove decisive. Compared with just four years ago, yields remain elevated enough to keep income attractive, but the range-bound behavior in the benchmark 10-year over the last two years suggests investors still do not have a clear answer on the next decisive move in rates.

Inflation is a big reason why. March CPI rose 0.9% from the prior month for a year over year increase of 3.3%, while Core PCE year over year was 2.97% in February, remaining well above the Fed’s 2% target level. Inflation’s “stickiness” is enough to explain why the Fed has not felt urgency to move, but still high enough to prevent a full-blown bond rally. One year ago, investors were more confident that inflation was gliding lower; this year, the message has been more stubborn. For Treasuries, that has kept front-end yields from falling much. For corporate and municipal bonds, it has meant carry remains appealing.

Growth, meanwhile, has cooled. Real GDP for the fourth quarter of 2025 was revised down to 0.5% annualized, a sharp slowdown from 4.4% in the third quarter. That is not recessionary on its face, but it does point to an economy that is losing momentum. Year to date, this softer growth backdrop has helped cap how far long Treasury yields have risen, even as inflation has stayed sticky. The next quarterly GDP release occurs at the end of this month where growth looks less robust. That is why the bond market has not treated higher inflation as a simple “rates straight up” story: slower GDP can push demand for duration.

The labor market sits in the middle of that tension. Job Openings (JOLTS), although down from their peak, remain higher than long term averages. Nonfarm Payrolls have bounced around while Labor Participation has fallen below long-term averages, indicating a hidden weakness. Still, the Unemployment Rate is healthy at 4.3%. Those figures suggest the labor market is softer than during its hottest phase but still not weak enough to prompt rapid Fed easing. For fixed income, that matters because a labor market that is cooling without cracking tends to anchor the intermediate part of the curve. Year to date, each employment report has mattered less as a recession alarm and more as a timing signal for when, or whether, the Fed can cut. Versus a year ago, labor is less inflationary but still firm enough to keep policymakers cautious.

Oil has been another important swing factor. Energy prices helped lift March CPI, but the recent drop in oil after the reopening of the Strait of Hormuz and ceasefire headlines has given markets some relief. That helps explain why equities have rallied even while bond yields remain relatively contained. The S&P 500 rose 3.3% in the week ended April 17 and had logged gains in 11 of the prior 12 sessions, showing that investors have recently leaned into the “growth slows, but not too much, and inflation may not reaccelerate further” narrative. For bond investors, lower oil prices are useful not because they solve inflation, but because they reduce one of the clearest near-term upside risks to inflation expectations.

In credit, the broad picture has been steadier than the macro headlines might suggest. U.S. Corporate Investment Grade Index yield of 4.97% is on top of its yearly 4.96% average. High-quality A and BBB-rated corporate spreads have also stayed steady although low relative to long term averages. That implies high-grade corporates have continued to offer meaningful income without showing the kind of spread stress that typically accompanies a genuine macro scare. Compared with one year ago, all-in yields remain attractive, even if spread compression is less of the story than simple income.

Municipals tell a similar story with yields as a percentage of Treasuries inching higher on the year but relatively low versus long term averages. However, elevated Treasury rates keep nominal yields attractive especially out on the curve. The municipal curve displays steep upward slope in particular for mid to long-term maturities. Year over year, market activity remains healthy, which supports the idea that municipal bonds are still being used as a core allocation. Any move higher has been met with tremendous investor appetite.

The main takeaway is that 2026 has not been a year of dramatic fixed-income repricing so much as a year of stubborn equilibrium. Inflation has stayed sticky rather than collapsing. Growth has slowed rather than rolled over. Labor markets are weaker but not weak. The Fed has stayed patient rather than pivoting aggressively. The result is a Treasury market in a fairly tight range, corporate and municipal markets that still offer respectable income, and an equity market that has recently been willing to look through macro uncertainty. For investors, that means the fixed-income case remains less about chasing a big duration call and more about harvesting income while staying disciplined about quality, maturity, and the possibility that the next big move in rates still depends on whichever side of the inflation-versus-growth debate finally gives way.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.